We've seen the market drop precipitously only to experience the best 50 day run in history. Meanwhile, new unemployment numbers are in the millions and increasing each week. The dichotomy of between what's happening on Wall Street and Main Street has arguably never been as stark as it is now.

If you've been exposed in 2020 by a lack of liquidity (access to cash) and seen your overall net worth drop by greater than 15% in 30 day time frame, then now is the perfect time to rethink and reshape the foundation to your financial plan.

There are critical elements this pandemic has exposed in the traditional financial model. For the purpose of this article I'm going to focus on one area you probably give little thought to:

Your Savings Strategy

First...

What does your savings strategy look like?

Do you save in a traditional bank? Is your savings really an investment plan like a 401k?

These are important questions because whether you save your money in a bank or a government qualified retirement account, you've exposed your money to at least of 1 of the 3 main Wealth Destroyers that are eating away at your net worth.

3 Wealth Destroyers

- Risk: Can you lose money?

- Taxes: How much of the growth do you keep?

- Inflation: Are you staying ahead of the invisible tax that reduces your purchasing power?

(There's also a 4th Wealth Destroyer which I'll get to in a moment)

Second...

Does your savings strategy make you more accountable, more efficient, and more profitable?

Let me ask you in a different way so you can better understanding of what I mean.

How much value do you place on cash?

For most people, the value is very low.

For most people, the value is very low.

If you pay cash for large items, you likely don't save money on a planned schedule. You simply save what's necessary for your next big purchase or emergency. This is important because not having a systemized plan means you place very little value on your saved dollars.

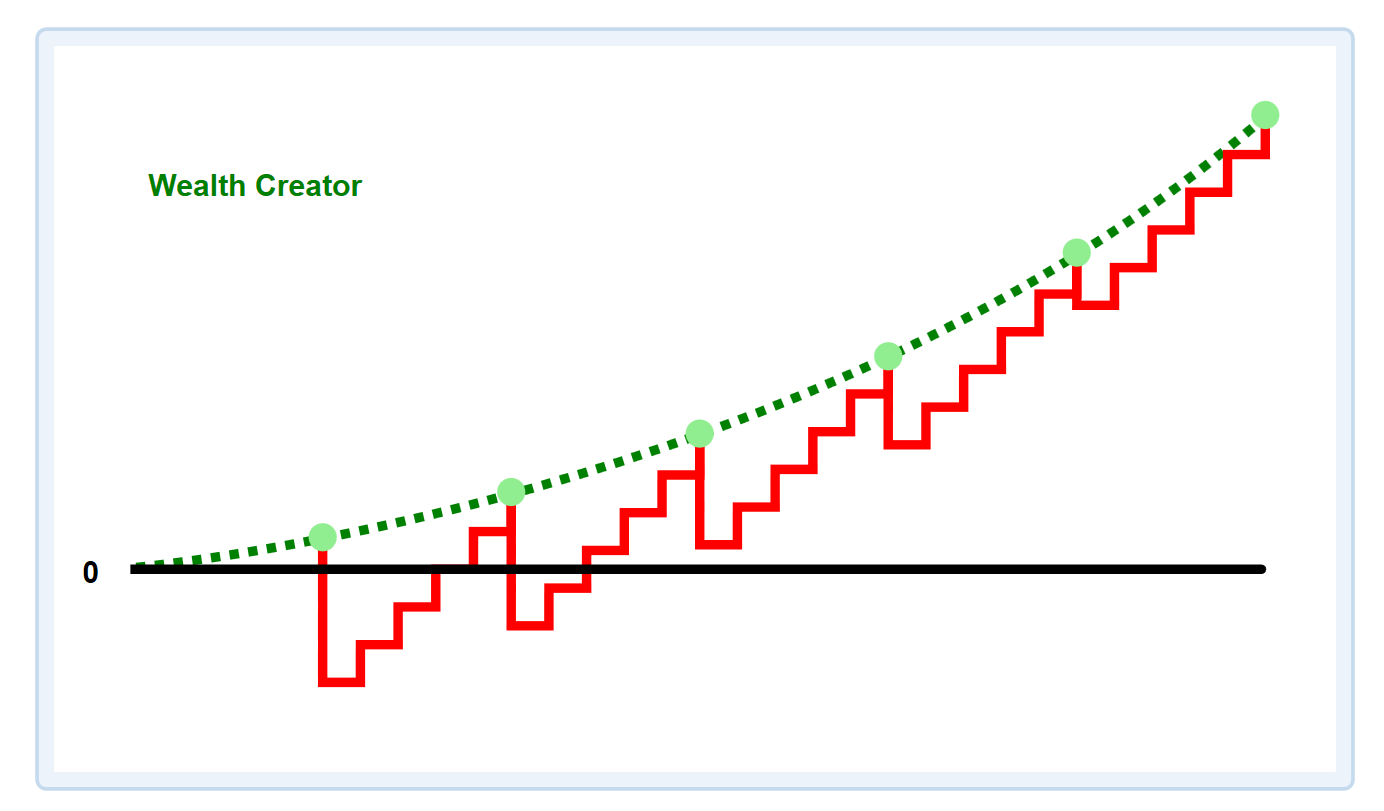

Think of it this way, when you borrow money from a traditional bank, you pay interest. If you save money, you expect to earn interest. Yet, when you use your saved dollars, you don't put any value on that money but this is a HUGE MISTAKE because of the opportunity cost of paying with cash from your traditional accounts.

Remember, you either pay or earn interest. Paying with cash means you give up the ability to earn interest on that cash forever, and this is true even if you are great at replenishing your savings account!

You save up, spend, and start all over. Rinse, Repeat. It looks like this:

Remember, you either pay or earn interest. Paying with cash means you give up the ability to earn interest on that cash forever, and this is true even if you are great at replenishing your savings account!

You save up, spend, and start all over. Rinse, Repeat. It looks like this:

Let's now plug a high early cash value (Infinite Banking) Whole Life policy into the equation and see how it holds up to the 3 previously mentioned Wealth Destroyers.

- IBC Whole Life policies eliminate market risk,

- IBC Whole Life policies remove the taxes on the growth, use, and transfer of those dollars,

- Cash Values (and the future death benefit) are increasing at a pace that stays ahead of inflation,

and you have a Savings Strategy that incorporates an asset class that overcomes the 4th Wealth Destroyer:

The Constant Interruption of Growth

If you don't think this is important, ask yourself this:

How much money will pass through your checking/savings account in your lifetime never to be seen again? It's a large amount of money, am I right?!? Wouldn't it make sense to allow that money to work for you all of your life rather than disappear forever?

When you use cash value to fund your lifestyle, pay for your kid's education, start or grow a business, or even prepare for retirement, you own an asset that you can use and re-use without interrupting the compounding curve of your saved dollars.

This is because cash values continue to grow on the full value even when there are loans taken. You can't get uninterrupted growth with a traditonal bank account or 401k/IRA.

How much money will pass through your checking/savings account in your lifetime never to be seen again? It's a large amount of money, am I right?!? Wouldn't it make sense to allow that money to work for you all of your life rather than disappear forever?

When you use cash value to fund your lifestyle, pay for your kid's education, start or grow a business, or even prepare for retirement, you own an asset that you can use and re-use without interrupting the compounding curve of your saved dollars.

This is because cash values continue to grow on the full value even when there are loans taken. You can't get uninterrupted growth with a traditonal bank account or 401k/IRA.

But to really make IBC work, you need to be accountable to your wealth!

A little discussed benefit to having an Infinite Banking Whole Life policy is how the use of this type of Savings Strategy makes you more accountable, efficient, and even more profitable than the traditional savings plan you currently use.

A little discussed benefit to having an Infinite Banking Whole Life policy is how the use of this type of Savings Strategy makes you more accountable, efficient, and even more profitable than the traditional savings plan you currently use.

People who don't understand how cash value life insurance works scoff at the notion of taking policy loans because they place little to no value on their saved dollars. They don't know what they don't know...

Utilizing policy loans are critical to building your net worth because taking and repaying policy loans forces you to be accountable to your money, including when you use the cash values for investing.

On the point of using IBC for investing, my IBC Whole Life policies don't restrict me from making investments. On the contrary, accessing the cash value via policy loans have made my investments more profitable by using leverage available in Whole Life policies to create two assets from the same dollar.

Here's the main point:

On the point of using IBC for investing, my IBC Whole Life policies don't restrict me from making investments. On the contrary, accessing the cash value via policy loans have made my investments more profitable by using leverage available in Whole Life policies to create two assets from the same dollar.

Here's the main point:

IBC forces you to replenish your wealth so that you never liquidate your savings without any intention of keeping it growing.

If you are serious about accumulating wealth that can overcome all 4 Wealth Destroyers, it's imperative you evaluate your current savings strategy to be sure you setting the proper foundation for building wealth that can endure any financial storm.

And don't forget, just because a Whole Life policy is an unmanaged asset (it has guarantees and it can't lose money based on market whims), "practicing IBC" means you need to practice being accountable to the dollars you save!

Chances are you are already a good Saver. You're just not saving in the best spot!

And don't forget, just because a Whole Life policy is an unmanaged asset (it has guarantees and it can't lose money based on market whims), "practicing IBC" means you need to practice being accountable to the dollars you save!

Chances are you are already a good Saver. You're just not saving in the best spot!

If you have questions about your current IBC plan or are looking to get started with IBC, you can connect with me here: www.IBC.guru.

Thank you,

John A. Montoya

John A. Montoya

No comments:

Post a Comment